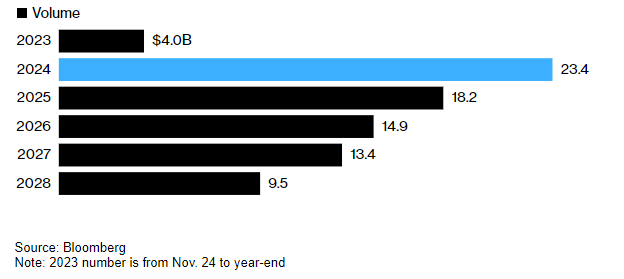

Private credit lenders are circling distressed property developers in Hong Kong, with a record $23.4 billion of bank loans coming due next year for the downtrodden sector.

The potential funding gap is drawing a range of players — including family offices, private equity firms and asset managers, such as PACM Group Holdings Ltd. — who can stomach offering high-risk, high-yield loans for collateral in one of the world’s most expensive property markets.

“There are family offices and asset management companies which are establishing this new business line just as private credit funds,” said Jasmine Chiu, a Hong Kong-based lawyer in real estate finance practice for Mayer Brown LLP. “They all seek to increase their portfolios for private credit.”

The opportunity is underpinned by Hong Kong’s listless market conditions, with revenues from office buildings and retail space weakening just as finance costs surge. While the city’s real estate sector has not undergone anything near the crash in China, homes sales have plunged and vacancy rates have soared. Many developers operate on both sides of the border, and cratering valuations in the world’s second-largest economy have had spillover effects.

Issuance details of private loans are often confidential, but there are recent deals pointing to the returns and demand. Agile Group Holdings Ltd. borrowed up to HK$894 million ($114 million) at 20% interest, while Flow Capital (HK) Ltd. offered a HK$900 million ($115 million) loan to a unit of distressed developer Country Garden Holdings Co. earlier this year.Some of Chiu’s private equity clients that have dabbled in commercial properties have switched to become private credit lenders, she said.

More non-bank financing would allow developers to quickly pay for new projects or refinance loans — as cash flows dry up — but the higher interest rates would add to the industry’s debt-driven woes. Even some of Hong Kong’s biggest developers, such as New World Development Co., are seeking to cut borrowings after aggressive expansions.

Asset-Backed Lending

Lenders see opportunities in Hong Kong in asset-backed lending, a fast-growing area in private credit in which borrowers put up specific properties as collateral. In launching a $300 million fund, Hong Kong-based PACM partnered with local financier Oi Wah Pawnshop Credit Holdings Ltd., with a focus on debt backed by real estate.

CBRE Group Inc.’s Hong Kong team has evaluated more than 30 high-yield private credit deals backed by assets including office buildings, data centers, and luxury homes, according to Keith Tsang, executive director of investment banking for Hong Kong at CBRE.

“It’s a double whammy where your cost of finance is going up, (and) your valuation’s coming down,” Tsang said. Private credit borrowers in Hong Kong have “become more and more distressed.”

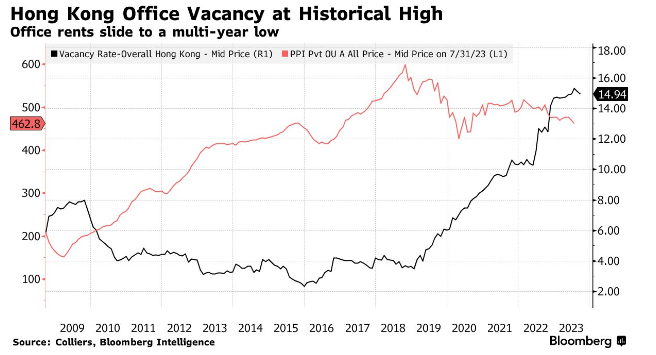

The downturn is severe. The vacancy rate for commercial space was close to a historical high at 15.8% in the three months to September, according to CBRE. An office building majority held by Goldman Sachs Group Inc. cut its asking price by more than 30%. Home sales volume last month fell 33% from a year earlier.

Hong Kong Property Developer Loans Face Maturity Wall

There’s $23.4 billion-equivalent coming due by the end of next year

Still Expensive

Still, market watchers say the Hong Kong private credit market is in its nascent phase — with more inquiries than completed deals. Some lenders are concerned that returns may come below their targets as many property assets still show resiliency and aren’t yet repriced, according to people with knowledge of the matter. They asked not to be identified discussing private deals.

“There are special situation investment opportunities in Hong Kong’s real estate market,” said Kei Chua, partner at Bain Capital Special Situations in Hong Kong. “But Hong Kong assets have always been expensive. The yields most of these deals offer are still few and far between our targeted returns.”

Conditions may change abruptly next year as banks will have to undergo asset-repricing in the first quarter to report annual results.

Private credit funds will be on the lookout for signs that — as distress cases rise and asset prices fall — banks may be prompted to sell their loans at a discount before they become delinquent. That would likely drive more borrowers to scour for other funding.

“The kind of second-, third-tier developers or fund managers owning assets in that kind of second-tier level, you’re gonna see a lot of challenges in the months ahead,” CBRE’s Tsang said.